All businesses in the UAE must register for corporate tax from June 2023 onwards.

• All business will be subject to corporate tax from first financial year starting on or after 1 June 2023.

• Every business needs to register for corporate tax, including free zone companies & freelancers.

• Corporate tax is separate from VAT. Even if you already have a VAT number, you need to register for corporate tax.

Keep proper accounting records.

• UAE’s corporate tax law requires specific accounting records to be kept.

• Your company’s tax obligations will depend on what your accounting records say about your business.

If you are exempt from corporate tax or if you qualify for the Small Business Relief rule, your accounting records must support your position.

File a corporate tax submission with the Federal Tax Authority (FTA).

• This step needs to be done after the end of your first taxable period.

• Even if you qualify for an exemption or tax relief, you still need to declare this by filing a tax submission with the FTA.

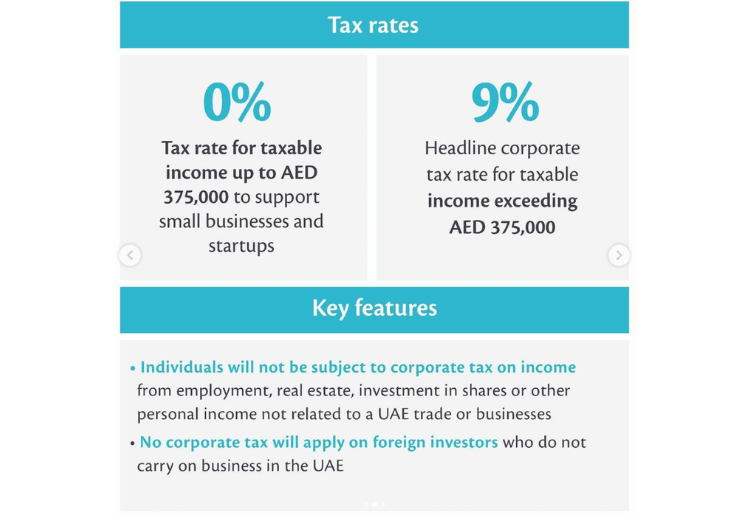

How much is the corporate tax in the UAE?

The Ministry of Finance (MOF) has developed a taxation policy with three tiers:

TIER 1

0% Tax Rate

Businesses with annual net profits of up to AED 375,000 are subject to a 0% tax rate.

TIER 2

9% Tax Rate

Businesses are subject to a 9% tax rate on annual net profits that exceed AED 375,000.

TIER 3

Different Tax Rate

Large multinational companies may be subject to a higher tax rate, subject to Pillar Two of the Organisation for Economic Cooperation and Development (OECD) base erosion and profit shifting (BEPS) project. Companies with a total global revenue of over EUR 750 million (around AED 3.15 billion) will belong to this category.

-

PROFITS UP TO AED 375,000 = 0% Tax Rate

-

PROFITS OVER AED 375,000 = 9% Tax Rate

-

PROFITS OVER AED 3.5 billion = Higher Tax Rate

Corporate tax for free zone businesses

To uphold its commitment to facilitate a business-friendly environment in the free zones, the UAE government has made an exception for businesses incorporated in free zones.

IMPORTANT: A business registered in a free zone is not automatically exempt from corporate tax.

Corporate tax policy for free zone businesses

If a free zone business complies with its free zone’s regulations, including those specified in the corporate tax legislation, they may qualify for an exemption.

If a business does not comply with the free zone conditions included in the tax legislation, they may lose their exemption.

If a business loses their free zone exemption, they may still qualify for other options available such as the Small Business Relief rule.

Remember that even if a free zone business qualifies for an exemption, they will still need to register for corporate tax, keep proper accounting records, and file an annual tax submission with FTA.

Corporate tax for freelancers

To practise as an independent professional or freelancer in the UAE, you need a professional licence, which will automatically bring you under the tax regulations.

If you are a freelancer whose annual revenue is over AED 3 million and profit is over AED 375,000, you will likely have to pay the 9% corporate tax for the appropriate income amount, unless you qualify for one of the exemptions available.

Freelancers in the UAE may still need to pay the 9% corporate tax if their annual revenue is over AED 3 million and profit is over AED 375,000.

Does the Small Business Relief rule apply to you?

The Small Business Relief rule is designed to support start-ups, SMEs and micro businesses in the UAE by alleviating their corporate tax duties and compliance costs.

REVENUE UNDER AED 3 Million = No Tax

The Small Business Relief scheme specifies that businesses earning a total revenue of below AED 3 million for each tax period will not be required to pay corporate tax. This is available until the end of 2026.

How do you calculate your taxable profit?

Your taxable profit is normally your revenue less your business-related expenses.

Some expenses have specific rules around them, including:

Salaries paid to owners

The law states that payments to a related party must meet the “arms-length” principle. For business owners paying themselves a salary, this means setting the salary at a fair market rate, similar to what an unrelated employee would receive under a similar employment arrangement.

Interest

Businesses can deduct their financing and interest costs. However, the amount of interest expense that can be deducted is capped at 30% of earnings before interest, taxes, depreciation and amortization (EBITDA).

This cap has been put in place to prevent businesses from exploiting the different tax treatment of equity and debt, whereby a business may take on excessive levels of debt to reduce taxable income via increased interest expenses.

Entertainment

Only 50% of entertainment spending can be deducted. This includes costs such as meals and accommodation, where they are incurred entertaining customers, suppliers, shareholders or other similar parties.

Foreign branches

If a company has a branch in another country, they can claim a foreign tax credit for the amount of tax paid in that country in relation to that branch. Alternatively, a company may apply for an exemption of the profit made by their branches outside the UAE.

Exempt income sources

MOF has also announced that income from the following sources will be exempt under most circumstances:

- Dividends and other profit distributions received

- Capital gains from selling the shares of a subsidiary company under their ownership

Exempt industries

If a business or any legal entity fits any of the criteria below, then they can qualify for corporate tax exemption.

- Government or public entities

These include both federal and regional offices, departments, divisions and all other public institutions. - Businesses that extract or mine natural resources

Businesses that deal with the extraction or mining of natural resources in the UAE are already subject to Emirate- level taxation, so they don’t have to file a separate tax report. - Public or regulated private entities

These include entities that deal with social benefit funds like pension or retirement planning. - Real estate or regulated investment funds

Similar to charitable organisations, such funds must apply to MOF and FTA to obtain a formal exemption approval. - UAE Government- owned companies

UAE companies fully owned by the UAE government and listed with a ministry-level decision will receive tax exemption. - Charitable organisations

Entities working for charitable and social causes must register as such with MOF. Those eligible must first apply to relevant authorities to obtain a formal clearance before applying for MOF registration.

Is corporate tax the same as VAT?

Companies will have to pay corporate tax on their annual net profits, while businesses collect VAT from customers when selling a product or service and then remit it to the government.

IMPORTANT: Businesses that have already registered for VAT will still need to register for corporate tax.

VAT is a consumption tax levied on the sale of goods and services. The customer pays it at the time of purchase. On the other hand, corporate tax is levied on businesses’ taxable income.

Corporate tax will be paid directly to the government and calculated by considering the net income of the company, not the total revenue or sales volume.

If you have any questions, we advise you to contact a certified tax advisor or accountant.